The issue of ESIC contribution on arrears of wages continues to be one of the most debated compliance areas during inspections and assessments. Employers frequently face demands on retrospective wage revisions, increments, union settlements, and arrear payments — often leading to disputes on whether contribution is payable for the original wage period or only from the date of declaration.

A combined reading of the ESIC Revenue Manual, RTI clarification issued by ESIC, and judicial precedents provides significant clarity on this subject.

Situations Where Arrears Commonly Arise

Arrears of wages generally arise due to:

• Retrospective wage revisions,

• Annual increments sanctioned later,

• DA increases from back dates,

• Union settlements,

• Court awards or tribunal orders,

• Management decisions enhancing wages.

The central question is:

“When does ESIC contribution liability actually arise?”

ESIC Revenue Manual Position

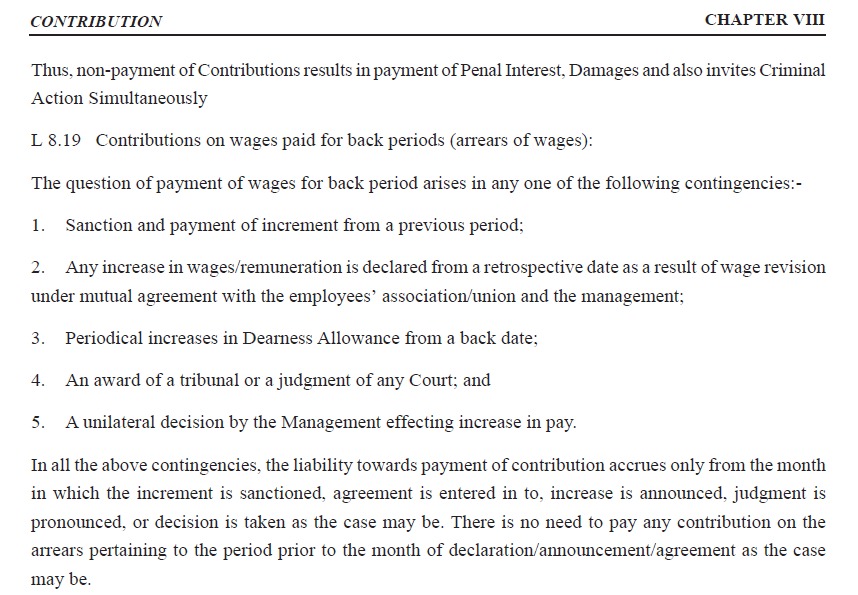

The ESIC Revenue Manual contains a very important clarification regarding “Contributions on wages paid for back periods (arrears of wages).”

It states that contribution liability accrues only from the month in which:

• increment is sanctioned,

• agreement is entered into,

• wage increase is announced,

• judgment is pronounced, or

• decision is taken.

The manual further clarifies that:

“No contribution is required on arrears pertaining to the period prior to the month of declaration, announcement, agreement, or decision.”

This distinction becomes extremely important in cases where wage revisions are given retrospective effect.

ESIC RTI Clarification – Surat Office

An RTI response issued by ESIC Surat Office in 2014 further reinforced this position.

The query specifically asked whether ESIC contribution is payable on arrears arising due to retrospective wage settlements.

The official response clarified:

• contribution liability arises only in the month in which the decision is announced; and

• no contribution is payable for the earlier retrospective period.

An illustration was also discussed:

If an increment is announced in October with retrospective effect from April, ESIC contribution would arise from October and not for April to September.

Landmark Judicial Support – Juliet Industries Ltd. vs ESIC

(Employees’ Insurance Court, Thane – 2021)

Facts of the Case

• Wage settlement with union executed on 17 July 2013,

• Settlement granted wage increase retrospectively from 1 January 2012,

• Employer paid arrears accordingly,

• ESIC demanded contribution for the retrospective period beginning January 2012.

The employer challenged the demand before the Employees’ Insurance Court.

Court’s Observations

The Court relied upon:

• ESIC Revenue Manual,

• ESIC circulars,

• established legal principles.

The Court held that:

• Contribution liability arises only from the month in which the settlement/agreement is executed.

• Contribution cannot be demanded for the prior retrospective period merely because wages were revised retrospectively.

• ESIC recovery proceedings initiated for earlier periods were illegal and liable to be quashed.

Important Compliance Takeaway

The distinction between:

• “effective date of wage revision”

and

• “date of declaration/agreement”

is extremely critical.

Under the principles emerging from the above documents:

• Wage revision declared in October → Contribution payable from October

• Revision effective retrospectively from April → No contribution for April–September

• Union settlement signed later → Liability arises from settlement month

• Court award passed later → Liability arises from judgment month

Practical Impact for Employers

This principle becomes highly relevant during:

• ESIC inspections,

• C-18 notices,

• retrospective wage settlements,

• annual increment cycles,

• arrear disbursements,

• union negotiations,

• payroll reconciliations.

Employers should ensure:

• proper documentation of settlement dates,

• board approvals,

• union agreements,

• announcement dates,

• payroll records,

• arrear computation sheets.

These records become crucial in defending avoidable ESIC demands.

Conclusion

The combined position emerging from:

• ESIC Revenue Manual,

• ESIC RTI clarification,

• judicial precedents,

strongly supports the view that:

“ESIC contribution on arrears arising due to retrospective wage revision is prospective in nature and not retrospectively recoverable for prior periods.”

Given the recurring disputes in this area, organizations should evaluate arrear payments carefully and maintain robust supporting documentation to mitigate litigation exposure.

Author:

Bhavik Chheda

Partner – Chheda Consultancy Services